|

|

Personal Property

Personal property is defined as possessions or interests, exclusive of real property, that may be easily transported or stored. Encumbrances on any item must be verified and deducted from the Gross Market Value in order to obtain the Net Market Value (NMV).

Motor Vehicles, Boats, Campers, Trailers and Mobile Homes

Exempt

One motor vehicle, either an automobile, motor home or motorcycle, may be exempted. This includes vehicles which are unregistered, inoperable or in need of repair. If the client has more than one vehicle, he/she may choose which vehicle to exempt. It is NOT required that the exempt motor vehicle be used for transportation, currently registered and/or in working condition.

Note: Recreational and commercial vehicles are only considered exempt if other vehicles are not available.

Nonexempt

All other vehicles are considered countable property. Include the Net Market Value (NMV) in the property reserve. This includes boats, campers and trailers.

Exception: A motor vehicle used as a principal residence is exempt.

Determination of Value

SSBS must determine a reasonable value for motor vehicles. Some of the methods which may be used to determine the reasonable value include, but are not limited to:

- The market value determined by Kelley Blue Book.

- The market value determined by the “National Auto Dealers Association (NADA) Guide.

- Department of Motor Vehicle (DMV) License Fee Rate Table.

- An estimate of the Market Value obtained by the client from a disinterested, knowledgeable source.

Determination of Value Using DMV License Fee Rate Table

The DMV License Fee Rate (VLF) value is determined by the DMV and not by the Department of Health Care Services. Follow the steps below to determine the value of a vehicle.

- Enter the DMV Class Code and Year/Asterisk Year on the Property History Detail page in CalSAWS.

- The VLF Value will populate based on the information entered, and the SSBS should manually enter the value in the Fair Market Value field.

Note: When determining the value of a motor vehicle that is specially equipped for a disabled individual (i.e. wheelchair lift), the special adaptive equipment is not considered to increase the value of the vehicle.

Cash

Exempt

The client’s current month’s income is not counted as cash on hand.

Savings of a child from exempt earnings for future educational or other needs are exempt.

Nonexempt

All other cash in the possession of the client not already exempted.

Verification

Statements made about cash on hand can be verified by client statement unless the information is questionable.

Bank Accounts

Exempt

The amount of money in a client’s bank account that was deposited as current income is exempt. The bank statement must clearly show that the client’s income (e.g. Social Security income, etc.) is being directly deposited monthly, or a clear description of deposit indicates the client’s monthly income, then the identifiable current month’s income should not be counted as property.

The amount of money which the client can establish as the property of a person who is not a family member is exempt.

Proceeds from the sale of real property retained by the client if used to purchase a home or apply to the balance due on a home already purchased within six months of the date of the sale or date of application for MC (whichever is later) is exempt.

Note: The purchase of a home would include cost of moving, necessary furnishings, and repair or alteration to home.

Nonexempt

All other funds not listed in the exempt section above.

Verification

- Bank statement.

- A signed statement from the bank on bank stationery, including the account number.

- An ATM receipt (as a temporary verification) when the last routine bank statement is not current and the client is waiting for a new statement.

Any bank statement on file less than 90 days old can be used as verification at both Intake and Continuing.

Note: Money held in digital accounts (Venmo, PayPal, crypto, etc.) are considered liquid properties and value should be determined as appropriate.

CalAble Program / Accounts

A CalABLE account is a tax-advantage savings account that allows disabled individuals to save up to $15,000 per year and up to the lifetime maximum of $529,000 without losing their Medi-Cal benefits.

Treatment of CalABLE Accounts

Funds in a CalABLE account are not counted as property for MC eligibility purposes. In addition, all CalABLE account earning (i.e. interest and dividends) are not counted as income. Income received and deposited into a CalABLE account is however still countable income.

Distributions from a CaABLE account are not counted as income for MC eligibility purposes if used for a “qualified disability expense.”

Verification

In order to verify the individual’s account is a CalABLE account they must provide a statement or document that identifies the ABLE program. The document must list the following information:

- Name of the individual

- Account number

- Account open and closed dates

- Current account balance

Direct Express Cards

Direct Express cards are issued to individuals receiving federal benefit payments such as Social Security, Supplemental Security income and Veterans benefits.

Verification

The Direct Express card is linked to a financial institution and an account statement is required to be provided as verification of the balance. Statements are available online and can be both viewed and printed for free. The client may also request to have a monthly statement mailed to them at a cost of .75 cents per month.

Treatment of Direct Express Card/Account

The amount deposited each month is considered income in the month of receipt and the remaining balance is considered property.

Certificate of Deposit

Only the cash value of the Certificate of Deposit if liquidated at that time is considered countable property. Any penalties incurred are considered an encumbrance.

Stocks, Bonds, Mutual Funds

Exempt

Shares of stock in a village corporation held by natives of Alaska are exempt.

Nonexempt

All other funds not listed in the exempt section above.

Verification

Obtain the certificate. If unable to determine value, obtain a signed statement from the issuing institution showing a description of the investment and the number of shares owned.

Determination of Value

Verify using the most current statement or other official documentation of the value of the stock, bond, or mutual fund.

Oil Leases and Mineral Rights

All Oil Leases and Mineral Rights are considered countable property.

Verification

Obtain the certificate or other official documentation verifying the value.

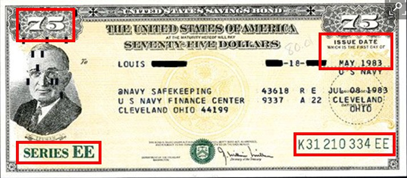

Savings Bonds

All U.S. savings bonds are considered nonexempt personal property.

Determination of Value

To determine the value of a savings bondsavings bond, go to the Treasury Savings Bond Calculator and enter the following:

- Value as of: Enter current Month and Year.

- Series: The Series noted on the bond (EE Bonds, I Bonds, E Bonds, Saving Notes).

- Denomination: Dollar amount of the bond.

- Bond Serial Number: The serial number on the bond.

- Issue Date: The issue date on the bond.

Trust Deeds, Mortgages, Notes, RAMs

Exempt

Deeds of trust, mortgages and promissory notes are considered exempt as other real property only when received through the sale of real property owned by the applicant/recipient. If the net market value is $6,000 or less and utilization requirements are met, the property is exempt. If the net market value is over $6,000, the first $6,000 of the net market value is exempt and the excess is included in the property reserves if utilization requirements are met.

Nonexempt

Deeds of trust, mortgages and promissory notes are considered nonexempt property if:

- Not received through the sale of real property owned by the applicant or recipient AND can be sold or discounted.

- Is other real property and

- Over the property limit, or

- Within the property limit, but not meeting utilization requirements.

The interest portion of payments is unearned income. The principal portion is property, and may be spent down within any given month to retain property eligibility.

Home Equity Conversion Plans

Home Equity Conversion (HEC) Plans allow homeowners age 65 and over to convert the equity in their homes to cash, allowing elderly homeowners to increase their available monthly income.

Since these plans are loans requiring repayment, the proceeds are generally considered available property, however, some HEC plans may provide that part of the purchase price of the home be used to purchase an annuity payable to the homeowner for life, in which case, the annuity payments are counted as unearned income in the month of receipt (as noted below).

As there are many variations of these plans, each plan should be examined on an individual basis. The most common HEC plans are:

Reverse Annuity Mortgage (RAM)

RAMs allow a homeowner to borrow, through a formal mortgage contract, 60-80% of the appraised value of the home equity for a specified period of time. The homeowner receives funds periodically for the duration of the lending period. At the end of the lending period, the loan must be repaid. Some RAMs may provide that part of the equity of the home be used to purchase an annuity payable to the homeowner. Such payments are considered unearned income in the month of receipt.

Deferred Payment Loan (DPL)

DPLs are similar to RAMs but differ in the following ways:

- Rather than being used as supplemental monthly income, the proceeds from the DPL are used for some specific purpose, such as payment of property taxes, home repairs or personal expenses.

- The DPL is received from the lender in one lump sum rather than periodic payments.

- The DPL is secured by placing a lien on the property.

- The amount of the loan may be recovered from the estate upon the homeowner’s death.

Sale-Leaseback

Sale-Leaseback is an arrangement where an investor (buyer) purchases the home from an elderly person (seller) and as part of the sales agreement, leases the home back to the seller. The lease allows the seller to live in the home either for life or until a specified time. The buyer usually pays the seller a down payment and monthly installments on a interest-bearing promissory note.

- The interest on the note is considered unearned income in the month of receipt. If the note can be sold, it is counted as a resource.

- The buyer is responsible for payment of real estate taxes, major maintenance costs and casualty insurance. The value of these in-kind items is not considered In-Kind Support and Maintenance to the seller who is paying rent.

- The seller pays the buyer rent. If the payments on the note are greater than the rental fee, the difference minus the interest portion of the monthly payment is treated as cash on hand and included in the property reserve (i.e., monthly note payment minus rent minus interest portion of monthly note payment equals cash on hand).

Time Sale

An elderly homeowner contracts to sell his/her home upon their death. In the meantime, he/she retains title and the right of continued residence in the home. In effect, the homeowner retains a life estate.

The buyer usually agrees to pay property insurance, property taxes, and certain maintenance and repair costs, plus a monthly cash amount to the homeowner during his/her lifetime. These proceeds are considered property conversion whether paid in cash or in-kind.

Home Equity Line of Credit (HELOC)

is a loan in which the lender agrees to lend a certain amount where the collateral is the borrower’s equity in his/her house. HELOCs are not considered available property until the fund is withdrawn AND retained for a full calendar month. If the client fails to report the receipt of HELOC funds in a timely manner, a potential overpayment exists.

Value

Determine the value by following one of the procedures:

- Obtain documents from the lender which establishes the principal amount remaining, or

- Obtain an appraisal from a party qualified to appraise mortgages, notes, and annuities, or

- Make a telephone contact with a recognized broker who buys, sells or appraises such items.

Annuities may have a penalty for early withdrawal. Use only the amount that is available to the client, subtracting any penalties charged against the value.

Related Topics

Life Estate Interest (Personal Property)