|

|

Applicant Gross Income Test

[W&I Code 11267 and 11450.12]

At the time of application, an AU is not eligible for the current or future month if the total reported or anticipated gross income for that month exceeds MBSAC plus special needs. Gross income includes:

- Total gross earnings from employment - less $450 for each employed person.

- Disability Based Income.

- Net earnings from self-employment income - Allow the actual business deductions or the 40% disregard. Refer to Self-Employment.

- Child Support whether received directly by the client or collected by the county (less the $100 or $200 disregard).

- Unearned Income.

- Any other non-exempt income of persons in the "family" whose income must be counted towards the AU.

Exception to Applicant Gross Income Test

Former recipients whose cash aid was discontinued due to TSE earnings shall now be considered recipients when reapplying for benefits within three calendar months of the TSE ending. However, if an individual applies for CalWORKs after this three-month period has passed, he or she shall be considered an applicant for the purpose of CalWORKs eligibility.

Income Tests

The Applicant Gross Income Test and the 100 Hour Work Rule shall not be applied to the former TSE client who was discontinued due to income and is applying within three months of their TSE termination. The Recipient Net Income Test must be used for these clients.

Financial Ineligibility in Month of Application

When the AU is determined financially ineligible for the month of application, but the Social Services Benefits Specialist (SSBS) determines the AU will become financially eligible within 60 days of the application date, the SSBS MUST enter the reasonably anticipated income for the payment period in CalSAWS. If the AU is financially eligible for the second month, CalSAWS will approve aid for the AU on the 1st day of the second month. The grant amount will be based on the reasonably anticipated income for the next six months (including the month of approval).

|

If financially eligible in the 2nd month, AND... |

Then CalSAWS... |

|

CalFresh is approved in the month of application (1st month), |

|

|

CalFresh is NOT approved in the month of application (1st month), |

|

Computation of Applicant Gross Income Test

To determine if the family passes the Applicant Gross Income Test, the SSBS must follow these steps:

- Determine the applicant family (AU and Non-AU members) gross income, including earned, unearned, disability based, and self-employment income.

- Disregard up to $450 of earned income for each employed family member. The remainder equals the Net Non-exempt Income (NNI).

- Determine MBSAC plus Special Needs for family (AU and Non-AU members).

- Compare the figure obtained in Step 2 with Step 3.

- If the NNI (Step 2) exceeds the MBSAC plus Special Needs (Step 3), then the AU is ineligible.

- If the NNI (Step 2) is less than the MBSAC plus Special Needs (Step 3), then the AU has passed the Applicant Gross Income Test.

Examples of Applicant Gross Income Test

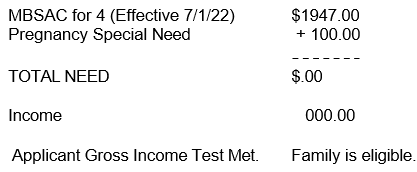

A family of four applies for CalWORKs in January. The mother is pregnant. The family has no income. The Applicant Gross Income Test is determined as follows:

If this AU has NNI (or is expected to receive income) in an amount in excess of $1788, the AU is not eligible.

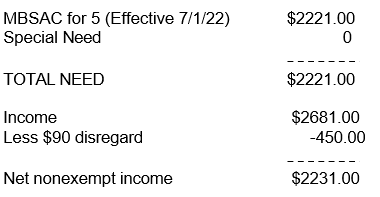

A family of five applies for CalWORKs. Mom is employed and earns $2,200 a month. The Applicant Gross Income Test is determined as follows:

The NNI is in excess of the total need for an AU of 5. They fail the Applicant Gross Income Test and the AU is ineligible.

Related Topics

Financial Eligibility Determination

Income Reporting Threshold (IRT)

Federal Financial Participation